Is Ultimate Products PLC (LON:ULTP) turning?

A mediocre business with some appealing qualities that is priced like garbage

Ultimate Products PLC (LON:ULTP) looks like an interesting situation. For 18 months, results have disappointed:

Source: Stockopedia

Consequently, the stock is very cheap:

Source: Stockopedia

Source: ShareScope

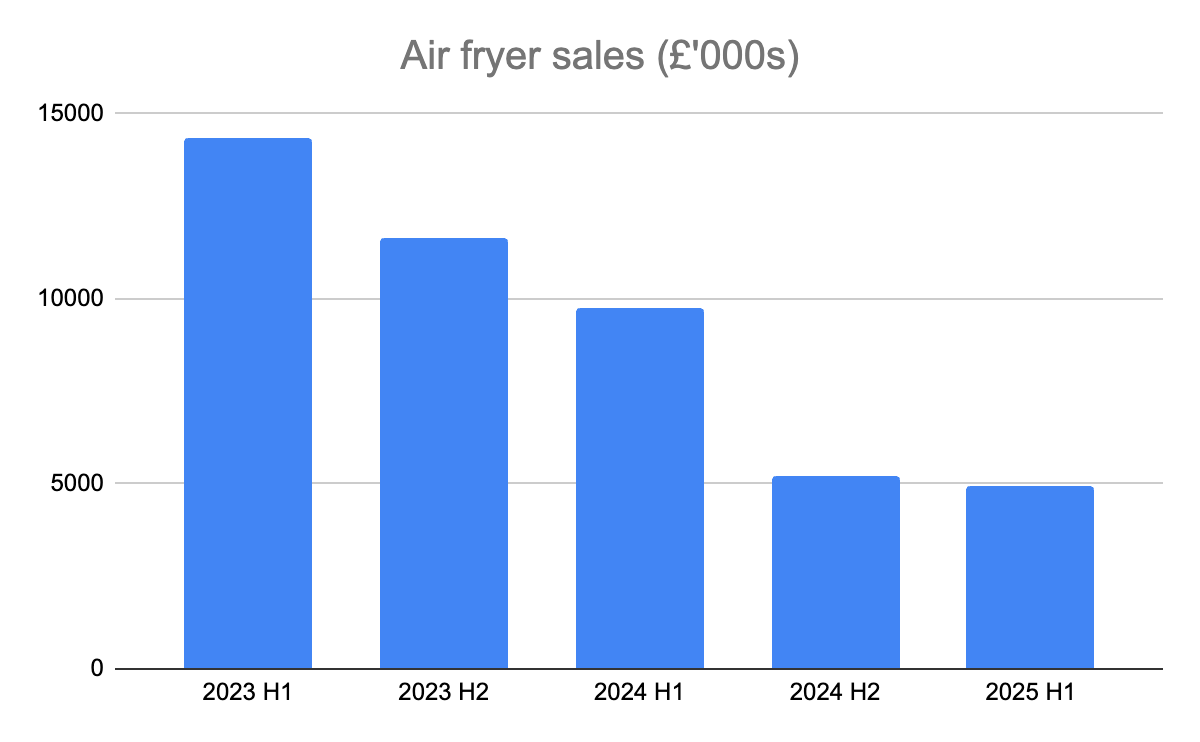

The primary reason for recent weak results relates to air fryers. As CEO Andrew Gossage explains in the 2024 Annual Report:

“In FY23, the widespread overstocking issues were mitigated by sales of our energy efficient products, particularly during the peak of the cost-of-living crisis in the Winter of 2023. This phenomenon was typified by our sales of air fryers, which performed exceptionally strongly during this period – reaching £26m of sales – but was unlikely to be repeated in successive years. In FY24, air fryer sales returned to a more normalised £15m, but remain at a significantly higher level than their pre-FY23 average. For example, H1 2022 sales were just £2.3m. As such, we are pleased to see that air fryers and other energy efficient products are now firmly embedded in everyday consumer behaviour, rather than being a passing fad.”

If we strip out air fryer sales from revenue over the past couple of years, we see that the underlying business has been stable:

Source: Ultimate Products financial reports

The company is guiding a return to revenue growth in H2 2025 and air fryer sales are unlikely to be such a drag going forward:

Source: Ultimate Products financial reports

The secondary reason for Ultimate Products poor performance was a spike in shipping costs which wiped out £2 million of profit in the first half of 2025. For context, group profit after tax was £10.5 million in 2024. There might be good reasons to expect continued volatility in shipping costs, but the H1 2025 profit impact was particularly pronounced.

Ultimate Products designs and sources household products from Asia and sells them under its own brands primarily to discounters and supermarkets. It is vulnerable to geopolitical shocks and is a price taker — personally, I have no interest in owning the company (again).

Two thirds of Ultimate’s sales come from the UK which is a fairly mature market, but it is having some success expanding in Europe. This provides a steady growth backdrop to a business which is sensitive to external factors (shipping costs, for example).

There are some other positives, too: it is founder led and has performed ok overall since listing in 2017. I think the stock is too cheap due to some temporary factors which appear to be waning and this is why I wanted to bring it to your attention.

Source: ShareScope

(I wrote a more detailed piece about Ultimate Products back in September 2022 on the Stockopedia website which I have copied below for those interested.)

Before I get stuck into UP Global Sourcing Holdings (LON:UPGS), I want to cover a recent sale. I sold Virgin Money UK (LON:VMUK) because I feared the impact on borrowers of the “cost of living crisis” but now suspect that I may have let my emotions get the better of me.

A major reason why I held Virgin Money was because rising interest rates should provide scope for banks to increase their net interest margin and indeed this appears to be the case based upon recent company updates.

In other words, the thesis was intact when I sold and my worry of an avalanche of loan defaults heading our way remains an unrealised risk that is looking more remote by the day given government willingness to bail-out all and sundry. And it really would take an avalanche of loan defaults to threaten Virgin Money since, like most of its peers, it boasts conservative capital ratios.

Still, in general I tend to shy away from banks because there is always uncertainty over the quality of their balance sheets and so perhaps it was the right call to sell Virgin Money due to questionable business resilience. Even if this was a case of letting my emotions get the better of me then that is ok, mistakes are inevitable.

I struggled to research UP because I simply don’t find the business particularly inspiring as it sells mundane homeware products such as mops and buckets, frying pans and weighing scales at budget prices. The unexciting nature of its wares is probably a good sign as it might explain an irrationally low price.

On the other hand, I have a nagging doubt about the quality of the business because it has cutthroat supermarket and discount retailer customers and little pricing power. This may prove particularly problematic in an inflationary environment and is another less encouraging possible reason why I struggled with motivation when researching.

Despite this misgiving, you may be surprised to hear that I have purchased shares in UP. I believe the group’s lack of pricing power is an acceptable weakness since it has maintained consistent gross margins over time, including during the past couple of covid plagued years.

UP manages rising costs through innovating new products at a rate of about 1,000 per year. Although it cannot easily increase the price of existing products, it can supersede them with higher priced versions with more bells and whistles.

Although UP isn’t the highest quality business, it does have a lot of desirable qualities and performance over the last couple of years during difficult times is evidence of resilience. I am also reassured by the longevity of many of their brands which significantly predate the group.

Management are disciplined capital allocators. They typically pay in the region of £100,000 to acquire brands which are often purchased out of administration. Cleaning products brand Beldray, founded in 1872 and the inventor of the fold-up ironing board, was acquired for such a figure in 2009 and now generates over £40 million in revenue.

I’m sure there is a long tail of brands which don’t make it, but the model works very well overall given the group’s high return on capital. I used EBITDA and average opening and closing capital employed in the below chart. Capital employed is net assets plus debt less cash. EBITDA is a decent proxy for pre-tax cash flow given the low capital requirements of the business.

The recent acquisition of Salter for £33.7 million using a mixture of equity and debt is another example of prudent capital allocation. A £15 million raising was done at £2.10 per share, a significant premium to today’s share price and close to all time highs. At the time of acquisition Salter was anticipated to contribute £4.6 million EBITDA in the year ending July 2022 and it appears that this was achieved based on preliminary results.

I believe that the acquisition of Salter is a watershed moment. The deal made sense on a number of levels. Firstly, UP had intimate knowledge of the company having sold Salter products under licence for the previous ten years with great success. Secondly, it is probably the most prestigious brand in UP’s stable being the oldest UK homewares brand with a 260 year history. Thirdly, under the previous licence UP was not able to sell Salter products in Europe where it sees huge growth potential going forward.

One of the things I like best about UP is its commitment to developing employees through its graduate scheme which was founded in 2012. Around half of the group’s 350 staff have come through the scheme and it is good to see that UP has a 4.4/5 rating on Glassdoor, the employee review site.

I believe that UP’s focus on its people is what enables it to compete. It managed to maintain 96% on-time delivery during the covid impacted period of the past couple of years despite sourcing a large proportion of products from China. It also launched over 2,000 new products during the period thanks to its inhouse product design and development team. It creates its own packaging which enables it to set its products apart from own-label alternatives.

In a recent presentation MD Andrew Gossage talked about UP’s systems enabling it to deliver where others can’t. He says that although they essentially just distribute products from factories in the developing world to retailers in Europe, there is significant complexity in doing so and that managing this complexity is what sets UP apart. He says that the major retailers like to keep things simple for themselves by shifting the complexity to suppliers such as UP.

A current project aims to automate many information processes using robotics and deliver significant efficiencies over time. 1,000 tasks have been identified and are being automated at a rate of 30 per week.

Andrew, who joined in 2006, owns a significant stake in the company as does founder and CEO, Simon Showman. Fellow founder, Barry Franks, recently stepped down from the board but retains the position of President. Between them, management owns about 50% of shares outstanding. That’s a lot of skin in the game as well as experience to back it up.

UP has come a long way since modest beginnings having been founded in Greater Manchester in 1997 as a clearance business buying discontinued and excess stock. The focus on brands was really cemented in 2013 following the acquisition of licences for Salter and Russell Hobbs in 2011.

Management have intimated that they expect to see substantial growth from the European business in coming years, particularly in Germany. Rolling out Salter to the European market is one lever, but there are also high hopes for recently acquired German brand Petra.

Petra was purchased for just £91,000 last year and was founded in Bavaria in 1968. It initially specialised in coffee making machines before expanding into other electric kitchen appliances. It is due to be relaunched in late 2022 or early 2023 with orders in hand from one of Germany’s largest hypermarket groups. Market research suggests that the brand remains well-known to German consumers despite a period of underinvestment from the prior owners.

Online growth is another focus for management with the target of achieving 30% of sales from this channel, up from 15% today. So far online sales have been via platforms such as Amazon and Ebay but the group recently launched a direct to consumer offering via the Salter brand.

Whilst there is no disputing the unrelenting growth trajectory of the group, not all financial metrics are so flattering. For instance, there is a history of inconsistent cash flow.

The reason for these fluctuations is that UP has fairly high working capital requirements and so the timing of payments has a large impact on annual cash flow. In addition, UP needs to invest in inventories and receivables as it grows. This is compounded by a shift towards supermarket customers since listing which have more stringent payment terms as well as a switch from FOB to landed arrangements with some customers (FOB has lower inventory requirements).

98% of receivables are insured which reduces the risk of failing to convert some of these assets into cash. The group also uses various flexible financing facilities to help cover the required investment in working capital as it grows. The inability to convert profits fully into cash from year to year is not an ideal situation, but the situation appears to be well managed and it hasn’t stopped UP from paying a consistent dividend of 50% of profits. If we encountered a similar liquidity crisis to the one we saw in 2008 then UP could be in trouble but I can’t see this being an issue in an inflationary environment with an accommodative government.

Overall gearing has increased due to the Salter acquisition but is reasonable at 1.3 times EBITDA according to the latest company update. Management have stated that they see no need to make further acquisitions currently given the abundance of organic growth opportunities at hand and so hopefully this will provide a chance to strengthen the balance sheet further.

Another potential negative worth noting is the disappointing results released in 2018 in the first year following listing when underlying EBITDA collapsed from £11.5 million to £6.5 million. Essentially, the issue appears to be related to a one-off switch from FOB to landed sales that year which created a timing lag in revenue recognition. The timing was far from ideal coming so soon after the IPO and the share price plummeted from a listing price of around £1.20 to the low 30s of pence. Since then both the shares and the group have performed well and so I’m inclined to look at the incident as a one-off.

Customer concentration is high with the two largest customers accounting for around 30% of sales but this is improving, falling from 45% at the time of IPO. I’m comfortable with this risk as I believe UP’s customers are becoming increasingly dependent on the service it provides. UP has proven itself to be a highly reliable partner during a time when many of its competitors would have struggled and it was recently awarded Supplier of the Year by Tesco. Supermarkets could invest in own-brands at the expense of UP but why would they when UP enables them to make decent margins without the hassle of managing things in house?

UP is also somewhat vulnerable from a supplier perspective and whilst it sources from 15 different countries, Chinese production is essential to the business. Management says that the group is actively seeking to diversify its supply chain away from China but that it will be a slow transition. Further deterioration of relations between the West and China is a risk to the business although one which would likely equally affect UP’s competitors such is China’s global trade dominance.

Chinese sourcing also brings with it currency risk given UP buys in US dollars and sells in pounds sterling and euros. The group is somewhat hedged and a 20% swing in rates would lead to a circa £1 million impact on profit according to the latest annual report which is nothing to get too worried about. Afterall, the group has successfully managed a period of soaring shipping costs combined with periodic Chinese lockdowns over the past couple of years and still managed to maintain consistent gross margins. I am hopeful that recent adverse currency moves will be similarly well handled.

I’m not keen on the management bonus structure which is based on EBITDA performance. EBITDA is not a statutory measure and there have been cases of companies using it to distract investors from their true inferior financial performance. I am somewhat comfortable with its use here since UP has minimal capital requirements and so excluding depreciation is not hiding anything but I would prefer a metric which also takes into account the shareholder equity and capital. This is because it is easy to grow EBTIDA simply by leveraging the balance sheet to make acquisitions or by diluting existing shareholders, neither of which necessarily lead to shareholder value creation. However, offsetting this risk is the fact that management owns so much of the business ensuring that interests are well aligned.

I am drawn to the simplicity of UP’s business model which is to provide quality branded products at own-brand price point. Through selling low ticket priced items of a semi-discretionary nature it should be somewhat protected from the challenging economic environment we find ourselves in. Management has been candid about the fact that the market is likely to shrink in the near-term but is confident in the group’s ability to take market share through continued expansion into Europe and leveraging its reputation for reliability and innovation. If it can do so while continuing to manage costs (as it always has done to date) then the current price-to-earnings multiple of around 7 represents very good value.