Portfolio update 1 June 2025

Weekly news and trading intentions featuring LON:INSE, LON:SAG, LON:CHRT & LON:GAW

Please bear in mind when reading this post that I own shares in most of the companies mentioned, which likely distorts my perspective. Also, the following content is for general information purposes only and is not advice. Please see the about page for my disclosure policy.

The UK investing portfolio, UK trading portfolio and Australian portfolio pages are all up to date as at COB on Friday.

It was half-term for my children this week and I spent most of the time looking after them. It was also a slow news week, which is probably not a coincidence.

Although I don’t provide regular updates for my trading portfolio anymore, I thought it was worth mentioning that I sold Spectra Systems (LON:SPSY).

On Tuesday, the company announced a change of its Finance Director. The prior CFO, Edward Spies, was appointed in May 2023, so not that long ago. There was no acknowledgement of his contribution to the company in the RNS announcing the appointment of his replacement, Kevin Richards.

The firm that audited Spectra’s accounts in 2023 is Miller Wachman LLP and their website doesn’t seem to be working at the time of writing.

EDIT: I just checked the link to the auditor’s website again at 2pm on 1/6/25 and the website is now functional. It was not working at the time when I published the article at 8am on 1/6/25 or when I wrote it on 31/5/25.

I’m not saying that anything untoward is happening here, just that I’m uncomfortable with the sudden change of finance director. I was holding Spectra in on a short-term basis, with a plan to sell into news of a potential future contract award. Given I am moving away from short term trading anyway, it was an easy decision to sell the stock and put the proceeds into Trustpilot Group (LON:TRST).

On Tuesday, Inspired PLC (LON:INSE), which is currently under a takeover offer from major shareholder Regent, revealed that mid-market US private equity firm HGGC was considering a cash offer of 81p for the company. This compares to Regent’s cash offer of 68.5p, plus a 1p dividend.

We already knew that Inspired was in negotiations with a third party, but did not know the potential alternative bidder’s identity or the price.

Through the course of the week we also found out that:

Regent has so far received acceptances representing just 0.1% of Inspired’s share capital. Regent currently holds 29.5% of Inspired’s share capital in total.

shareholders controlling 38% of Inspired’s share capital have indicated that they would accept an 81p offer from HGGC, should it arise.

It struck me as slightly odd (but perhaps it’s just me) that the following comment accompanied Inspired’s announcement revealing the details of HGGC’s potential offer:

“The person responsible for arranging this announcement on behalf of Inspired is Paul Connor, Chief Financial Officer.”

Unsurprisingly, I intend to wait and see how this plays out and will accept the highest offer that arises.

On Wednesday, Science Group PLC (LON:SAG) revealed an increase in its strategic investment in Ricardo (LON:RCDO) to 21.8% of the voting rights, up from 20.1% at the time of the AGM a week earlier.

In addition, Science released an open letter to Ricardo shareholders which, in my view, makes a very strong argument for voting for the removal of Ricardo’s chairman at the upcoming general meeting on 18 June.

If you want to read an analysis of the letter, then allow me to point you in the direction of fellow Science shareholder, Mark Allery. He also makes some observations about the quality of management at UK listed companies more generally. I agree with much of what he says, and not just because he complimented my substack.

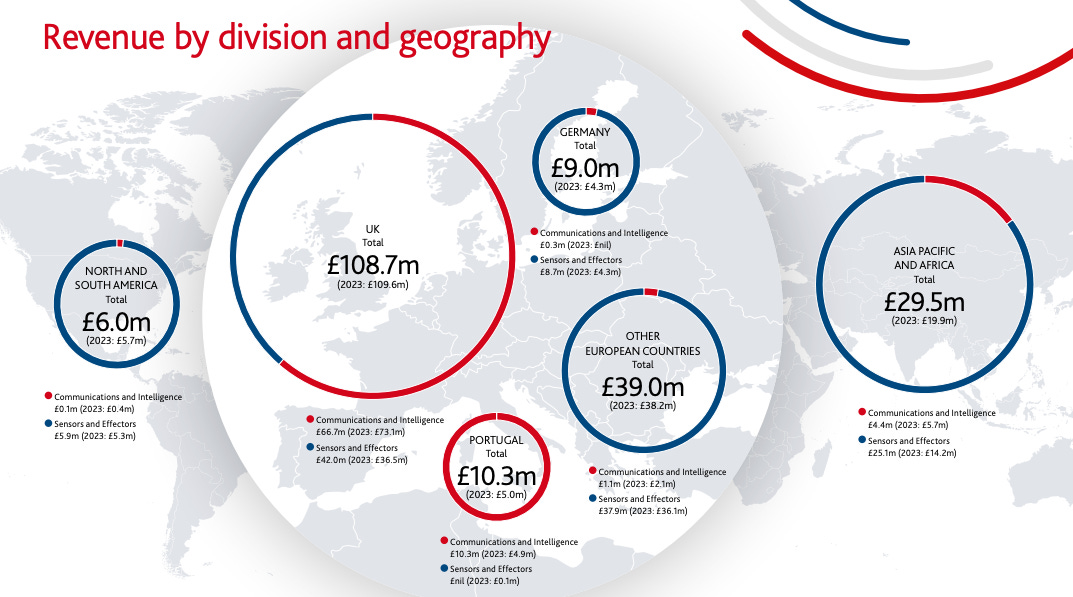

Cohort (LON:CHRT) released a full year trading update on Thursday and reported that profit was in line with market expectations for FY 2025.

Closing net funds were over £5 million and exceeded expectations. This represents a decline of around £18 million compared to last year’s closing position of £23 million.

However, Cohort purchased EM Solutions for £75 million during the year. Gross proceeds of £41 million were raised to part fund the acquisition, but that still leaves a ~£35 million shortfall. In addition, Cohort paid £3 million for the acquisition of Interactive Technical Solutions during the first half of the year.

Therefore, I estimate that the underlying cash build during the year was around £20 million, after paying ~£6 million in dividends. This compares to analyst consensus net profit for 2025 of £17.2 million according to Stockopedia and £20.4 million according to ShareScope.

In addition, Cohort closed the year with an all-time record order book of £615 million.

Cohort is my largest position and trades on a forward price-to-earnings ratio of 26 based on consensus forecasts for FY 2026. I am comfortable with this valuation because I think we are still in the fairly early stages of rising global defence spending, particularly within Europe.

Source: Cohort 2024 Annual Report

On Thursday, I visited my local gaming shop to learn more about Warhammer, the primarily tabletop game franchise owned by Games Workshop (LON:GAW). I chatted to the shop owner, who also plays Warhammer, for as long as my children would let me get away with.

Obviously, I did not get a complete insight into the full intricacies of Warhammer from this brief discussion. And I am somewhat hesitant to include this at all because I am aware that many readers have been Games Workshop shareholders for much longer than me and have a much better understanding of the business.

However (here’s your warning), this is my view on what makes Warhammer special.

I think that Warhammer benefits from what Charlie Munger called a “Lollapalooza effect”, meaning that multiple tendencies converge to create an extreme outcome. These are:

People like collecting things and Games Workshop has created many thousands of unique Warhammer figures over its 40 year plus history. The huge variety of options leads to highly personalised collections.

The pleasure and satisfaction derived from assembling and painting the models and the sunk cost of investing in paints and glue. The painting element further personalises Warhammer.

Games Workshop’s most popular game, Warhammer 40k, is based on a unique concept combining sci-fi and ancient history. This differentiates it from other fantasy games which typically draw on cliched ideas such as elves, wizards, witches, dwarves etc..

The rich and evolving “lore” which defines each Warhammer universe is laid out in hundreds of books with new ones released regularly. Each particular army, environment or campaign has a dedicated rules book called a codex. This depth and complexity keeps fans engrossed.

The face-to-face social element of playing a game of Warhammer which lasts several hours and is a combination of skill and luck. There was a two versus two battle being played while I was in the shop.

Limited editions and exclusive miniature releases mean that for some collectors, Warhammer is a Veblen good. Rare models can be highly sought after making them status symbols within the community.

There is a network effect, particularly within 40k, whereby more people are attracted to play the game because there are already many players to play with.

A large, engaged online community spreads the word and educates new players while enabling Games Workshop to remain attentive to customer demands.

That’s all for this week. Next week, I will be attending Oxford Nanopore Technologies’ AGM.