Returning to Oxford Nanopore (LON:ONT)

Bowing to those who know

Since writing about why I own Oxford Nanopore I have received some interesting feedback that is worth noting.

Positive for the thesis

Firstly, bioinformatician David Eccles took issue with the following comment from my original piece,

“right now it seems to me that the competition can do most of the things that Oxford Nanopore can”

You can read the full back and forth on Bluesky:

David has been calling Oxford Nanopore’s technology potentially disruptive since 2014. He appears to be an expert (although, who am I to judge?) and I defer to his superior understanding of the technology.

I was wrong to say in my original post that Oxford Nanopore was “laying it on a little thick” in some of its investor communications, particularly regarding its claims of being “disruptive”. Clearly, more enlightened observers than I am think that such statements are justified.

Despite this, I still reserve judgement as to whether Oxford Nanopore will ultimately eat Illumina’s lunch (which is what I originally had in mind over the question of disruption).

Oxford Nanopore is still to prove itself in the clinical market which is the largest market for genetic sequencing. The company generated clinical revenue of just £17.3 million in 2024, up 12% on the prior year. This is a paltry growth rate considering it is coming off such a low base.

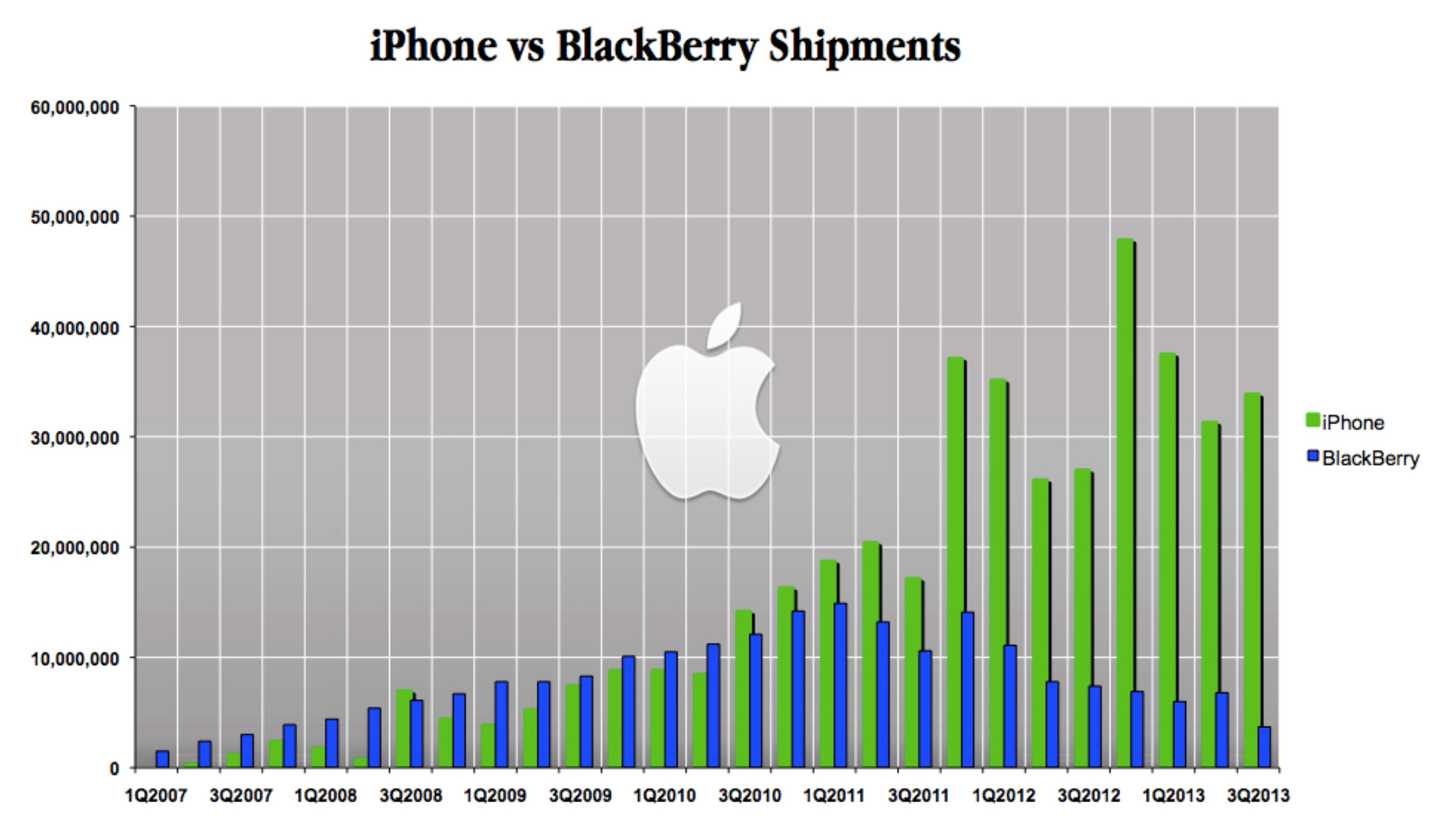

As David pointed out, “in order to dislodge, [Nanopore] needs to start somewhere” and these things can take time even the more violent of cases. For example, it was some years before BlackBerry felt the pain from the introduction of the iPhone.

Source: aaplinvestors.net

As an investor in Oxford Nanopore, I hope that David is right and this interaction has only strengthened my conviction in the company’s technology.

Negative for the thesis

In another ego shrinking episode, some better investors than me highlighted a risk regarding Oxford Nanopore’s share register which I missed in my original post. If you wish to indulge in some schadenfreude, then you can find the interaction on X (I don’t recommend it as schadenfreude is bad for your soul).

I originally wrote:

“It is quite unusual in my experience to have four large technology companies on the share register of a smaller peer. These sophisticated capital allocators may not be risking much as a proportion of their net worths, but they are likely to be well informed and to perceive substantial potential upside (why else would they be bothered?).”

What I missed is that for those who are stratospherically rich (such as top five richest man in the world Larry Ellison and Oxford Nanopore’s largest investor), a shareholding in Oxford Nanopore might represent a call option.

To such shareholders, the value of their holding is insignificant in terms of their total wealth which caps their downside as I noted in the original article. The part I missed is that they may not have to (or want to) fully share the spoils with little shareholders like me in an upside scenario because they have the means to take the company private before such spoils fully accrue.

I did touch on this in my conclusion when I said,

“Oxford Nanopore is at risk like predecessor Solexa of being gobbled up by a deep pocketed US group.”

However, I didn’t make the connection that the recent accumulation of stock on market by EIT Oxford Holdings (Ellison’s vehicle) might signal that such an outcome is on the immediate horizon.

To be clear, I am not saying the Larry Ellison or any party associated with him is planning to take Oxford Nanopore private. I have no idea, but he is rich enough to do so and has been recently increasing his stake.

This realisation does not make me want to sell my shares because I think Oxford Nanopore is worth far more than its current market price and I currently see little risk of failure despite it recording a large cash outflow last year.

Nonetheless, the lesson remains that it is simplistic to assume that the interests of sophisticated and powerful shareholders are fully aligned with my own. Unlike for those other holders, if Oxford Nanopore went to zero then I would feel it, and I don’t have the ability to take the company over if it looks like it will become as successful as I think it might.

One of the main reasons I started publicly journalling was to learn from others and so I am happy to be eating some humble pie, even if it doesn’t taste great.

Hello, have you checked the known short positions?

Ellison has been taking advantage of the shorts.

Some of the short hedges have also been shorting IPGroup[IPO] possibly because of their 10% exposure to ONT. It's pretty obvious that ONT's research income is going to fall thanks to Trump.

What will replace that income? It has to be clinical and industrial sectors.

Sanghera has gone on record to say that 2025 is the start of clinical income, and NHS placements are rapidly increasing. It's impossible to say how quickly these other income segments will make a meaningful contribution.