Portfolio update 7 June 2025

Weekly news and trading intentions featuring a long update on LON:ONT and a brief mention of LON:SPSY

I am resending this update to correct the comments about Spectra Systems (LON:SPSY) at the end. The reason that I could not access Spectra’s auditor’s website was related to my home internet connection. I have successfully accessed it using my phone connection and others have also been able to access it. Apologies for the mistake and please ignore the final comments about Spectra.

Please bear in mind when reading this post that I own shares in Oxford Nanopore, which likely distorts my perspective. Also, the following content represents my personal views only and is not investment advice. Please see the about page for my disclosure policy.

The UK investing portfolio, UK trading portfolio and Australian portfolio pages are all up to date as at COB on Friday.

I attended the Oxford Nanopore Technologies (LON:ONT) AGM on Wednesday, but before I get into the meeting, I want to lay out the reasons why I own the stock.

For background, I wrote a fairly long piece on Oxford Nanopore back in March, followed by a couple of points of review about a week later.

First up, I have no formal training or education in genetics or life sciences more generally. I am entirely unqualified to comment on the science which underpins Oxford Nanopore, but this is my diary and so I’m going to waffle on regardless with the hope that someone who knows what they are talking about corrects my mistakes. Therefore, don’t rely on the scientific content of this post.

You might be wondering why I invest in Oxford Nanopore given this is an area that is outside my circle of competence. Here are the main reasons (which are underpinned by my original articles on Oxford Nanopore):

The company has guided to profitability in the short to medium term (positive adjusted EBITDA by the end of 2027). Revenue is growing strongly and gross margins are rising which gives me confidence that this will be achieved, even if it takes a little longer than expected. Cash reserves look sufficient to get there, in my view. I think it is highly improbable that I’ll lose substantially all my money, unlike with typical binary outcome biotechs.

Sentiment within the biotechnology sector is pretty dire, following the normalisation in interest rates and the arrival of a heterodox administration in the White House — no bubble valuations here.

This is a well diversified, resilient business with 74% of revenue from consumable sales. The top five customers make up 8% of revenue and the split of research to applied customers was 70:30 in 2024, with applied markets growing much faster. 3,000 peer reviewed papers were published featuring Oxford Nanopore technology in 2024, with a total of over 14,000 to date. This is evidence of the breadth of applications for the technology which corresponds to the diversity of the customer base. I don’t need to worry about a small number of specialist use cases becoming obsolete, which my lack of technical knowledge would likely make it hard for me to see coming.

I broadly understand what makes Oxford Nanopore’s technology differentiated, and I have verified this view through independent opinions of those more knowledgable. There are only a small number of meaningful competitors to Oxford Nanopore and they are, broadly speaking, all at a disadvantage in terms of some combination of the strengths of Oxford Nanopore’s platform which are driving its growth (ie real-time, distributed, data-richness, long-read). This is a function of the way competing technology platforms fundamentally work (see my original articles on ONT), and so it seems likely to me that Oxford Nanopore has an enduring advantage in these areas.

These advantages are finally starting to feed through into the applied setting. This is why Oxford Nanopore is guiding for at least 20% revenue growth in 2025, despite an expected loss of NIH funding corresponding to 10% to 15% of the existing business. In contrast, key competitors PacBio and Illumina are guiding to a single digit percentage revenue increase and a slight decline, respectively.

Oxford Nanopore is adopting a partnership strategy to tackle applied markets and there are signs that this is starting to pay off. When asked what the company wanted to be when it grew up at a recent Morgan Stanley Analyst Fireside Chat, CEO Gordon Sanghera replied “Intel Inside”. From where I’m standing (somewhere right near the back of the room with an obscured field of vision), this strategy fits well and should enable the business to scale effectively.

Now, there are some criticisms that have been levelled at the company that I’ve read about. The following comment from computational biologist, Keith Robison, sums them up nicely:

“I often carp about their commercialization - the silly splitting of ordering and account management on two websites, the lack of next-day delivery of consumables, past problems with delivering wrong versions of kits, a too complex product lineup with poor documentation and guidance, a confusing user community as an utterly inadequate substitute for professionally written and organized materials - sure, I can lay it on.”

An independent view along similar lines can be found here. I take it at face value that such bugbears are justified, but even so they they are fixable and far from existential.

In addition, Keith has written a piece on recently departed CTO Clive Brown which, among other things, presents a picture of the company’s R&D focus during Clive’s time:

“Clive's passions and ethos of the individual explorer sometimes took the company in directions that were of questionable commercial relevance.”

This brings me to recent communications from the company regarding its move into proteomics.

There are two elements to the story. By the end of the year, Oxford Nanopore is planning to release, on early access, a single peptide sequencing solution (peptides are building blocks of proteins) which it hopes will be a stepping stone towards eventual full de novo protein sequencing. Full de novo sequencing would enable direct complete protein sequencing including post translational modifications and the identification of new proteins.

The single peptide solution is well advanced, but the market potential is unclear. While proteomics is a huge market overall, bigger than genomics, I do not know what proportion this initial nanopore application can address. However, perhaps there is potential within peptide biomarker diagnostics, given the nanopore solution can achieve an order of magnitude higher sensitivity than existing mass spectrometry techniques.

You can watch a video of CSO, Lakmal Jayasinghe, presenting the single peptide application here. Among other things, he presents data showing accurate identification of 12 peptide biomarkers related to various diseases using nanopore technology.

Crucially, Lakmal addresses a key challenge of proteomics being the vast dynamic range of proteomes. This means that within the same cell there can be a handful of one particular type of protein and ten million of another. That Oxford Nanopore’s peptide application can address this challenge adds credibility to the company’s proteomics ambitions.

The de novo solution remains a distant goal, for now. But over the longterm, there is the potential for Oxford Nanopore to bring the same advantages to proteomics as it has to genomics (high throughout, distributed, real-time, data richness). And the company would be able to use its existing hardware to do it, potentially just replacing the nanopore within the flowcell.

Once again, Keith Robison raises an interesting question about the extent of the overlap between potential proteomics customers and Oxford Nanopore’s existing customer base:

“For KOLs and customers, many of these spaces have weak overlaps. You'll always find some biological polymath or an unfocused company which will cross them, but in general scientists performing large scale genomic studies are a different population than those performing large scale DNA synthesis who are in turn different from those interesting in committing to exploring DNA-based data storage - and very few individuals from any of these groups are going to be interested in protein sequencing as it is likely to be realized by ONT.”

On this point, I noticed that at the recent London Calling conference when Oxford Nanopore collaborator Jeff Nivala asked the room if there were any mass spectrometrists (the primary instrument used for proteomics) present, it appeared as if there was no response. I asked Chief Product and Marketing Officer, Rosemary Dokos, about this following the AGM and she said that if he had asked who was interested in sequencing proteins, there would have been a large response.

She said that the company’s approach would be to release the single peptide sequencing solution to the community, who would hopefully then advocate on the company’s behalf once they had experienced the value of it. This is a similar approach to the way in which Oxford Nanopore gained traction with its original handheld MinION device ten years ago.

The fact that the company has already created a large customer base within the research community in genetics gives me confidence that it can do the same with proteomics, even if there is little existing overlap between these groups. Furthermore, a growing number of partnerships in the applied sector within genetics suggests to me that Oxford Nanopore could succeed with a similar approach within proteomics. Admittedly, I am unfamiliar with these groups and there may be significant differences between them which undermine these assumptions.

I asked a couple of questions during the meeting itself.

Firstly, I asked about the potential encroachment on Oxford Nanopore within applied markets (particularly regarding the business being won from Sanger sequencing) from Roche’s SBX technology, which can do slightly longer reads than Illumina (once again, hat tip to Keith Robison for introducing the concept of “midi reads”). The answer was that there wouldn’t be an impact given these applications either need longer reads than Roche’s capability, or require richer data, or are in a small batch size distributed setting.

Secondly, I asked about any impact from the new US administration on the business’s exposure to mRNA vaccines. The answer was that almost no revenue comes from these vaccines today, but that the company is in discussion with the major mRNA companies over potential partnerships.

Finally, I asked about the technical hurdles remaining before commercial launch of de novo protein sequencing, to which the answer was that more work was required on the unfolding enzyme, and the reader to improve resolution of certain amino acids. Gordon Sanghera said that overall, there was quite a lot of work still to do.

You may have seen that there was a significant vote against the re-appointment of chair, Duncan Tatton-Brown, with 34% voting against. My understanding is that entities associated with Oracle founder Larry Ellison, one of which (EIT Oxford Holdings) has been acquiring stock on market recently, hold about 18% of Oxford Nanopore in total. This represents Oxford Nanopore’s largest shareholding and so multiple parties must have voted against this resolution and they may or may not have included interests controlled by Ellison.

I note that Duncan Tatton-Brown lacks prior experience within the life sciences industry and so perhaps this explains the vote.

Alternatively, there could be a group agitating for a change of management with replacing the chair seen as a first step. Certainly, those shareholders who bought in at IPO are nursing heavy paper losses (-72% at the time of writing) and include Ellison. But this is no worse than other gene sequencing companies over this time and as I noted earlier, Oxford Nanopore is currently growing faster than its peers.

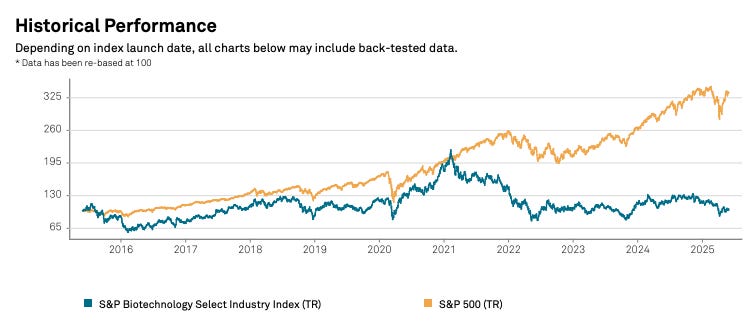

Source: ShareScope

The above chart begs the question as to whether the sequencing market is an “arms race”, whereby the eternal need to invest heavily in R&D to keep up means that no party is able to generate strong returns for investors. Under this scenario, as accuracy and data quality improves across the board, the market could become increasingly commoditised leading to companies competing on price in a “race to the bottom”.

This is certainly a risk, but I think that Oxford Nanopore is at least partially immune. It is improving gross margins while growing in a challenging market as its peers struggle, pointing to genuine product differentiation. We’ll have to see how the arrival of Roche plays out, but its technology currently lacks all of Oxford Nanopore’s key advantages (distributed, data rich, long read).

Given my view that the company has a bright longterm future, I hope that we don’t see a takeover of Oxford Nanopore in the near-term. But if Ellison’s recent share purchases do lead in an offer, it is unlikely be a bad outcome given he has acquired at prices above what I paid. If he wants to takeover the company, he will have to bid more than his highest purchase price of the past twelve months as per The Takeover Code.

In conclusion, I am comfortable holding Oxford Nanopore based purely on the progress it is making growing into applied markets within genetic sequencing. I can imagine Oxford Nanopore’s distributed platform, which enables rapid and cost-effective small batch size sequencing, thriving in the emerging era of personalised medicine. I am going to wait and see if I am right, and am positioned to profit if I am.

There is a risk that the move into proteomics proves to be an expensive diversion, but to my mind it represents a potentially highly lucrative and realistic opportunity. Given the size of the proteomics market, the upside is much larger than the downside, and the downside is limited by the fact the company can leverage its existing hardware. It is difficult to assess the likelihood of success, but the early release of the single peptide solution by the end of this year points to revenue generation in the near term. The longer term de novo ambitions are less certain, but there are reasons to think that nanopore sequencing can be successful here. In my view, proteomics represents a valuable option which is not priced in.

The votes against Duncan Tatton-Brown at the AGM indicate that there is some unrest among the shareholder base that extends beyond a single party. This could lead to a change in the board, and potentially the executive management team, and represents unwelcome uncertainty.

I respect the progress that the company has made under its current leadership and so am not personally clamouring for change. However, I can see why some might question certain decisions of the past and perceive less than perfect execution. Hopefully, even if there are executive changes, they don’t lead to a worse outcome for small shareholders like myself. I don’t think this will happen, with the possible exception of a lowball takeover.

Before signing off, I thought I’d mention that I have once again been unable to connect to Spectra Systems (LON:SPSY) auditor’s website. I wrote about this last week, and updated that article when I revisited the website of Miller Wachman LLP last Sunday afternoon to find that I could access it. Curiously, since then it seems to no longer be live.

EDIT 7/6/25: Others have told me that they can access Miller Wachman LLP’s website and so the fault is at my end. I did try multiple browsers before posting, but I think it is to do with my home internet connection because I have been able to access it using my phone. Apologies for the mistake.

In the coming week, I plan to attend the OXB AGM.

Impressed at the number of AGM’s you are able to attend Matt. Work and living location make this tricky for me and I wish I could attend more.

I also cannot access the website on any device or configuration. Most odd.